- How to start accounting for a start-up?

Accounting work starts with Cash Book and the procedure to use it.

If you are running a small business and want to use the manual method, enter all the transactions in a cash book or use Excel spreadsheets. A cash book has two sections: making payments is called debt, and receiving money is called credit. At the end of the month, when you receive the bank statements, you will check with your cash book and reconcile the accounts with bank statements; this is called bank reconciliation, which means the balance in the cash book should be the same as the month-end balance in the bank statement. But if you are using cash to make payments and receive cash, all that has to be recorded separately and maintained in a book called petty cash. Please update your cash book daily and balance it with the bank statements at the end of the month. It will have more control over finances than waiting until you receive the bank statements and then reconciling.

How to start accounting for a start-up?

Methods to preserve finance records.

- Firstly, separate your personal and financial records. Do not mix up bank and credit cards to save time and money; you will not need help to separate these records, especially for tax filing or inspection.

2. Transferring the surplus money to a particular account could be a savings account with easy accessibility in an emergency.

3. Maintain the files for all the sales invoices and purchase receipts, as you will need to buy equipment, computer, and software. Creating website expenses, hosting charges, and much more that support your business, as you must account for all these when the time is up for tax filing.

Choose an accounting method for small businesses.

As a new business, choose the accounting method to maintain accounts without hassle at tax-filing time. Using spreadsheet work takes a lot of time, and probably you, the business owner, might try to do that. Why not try that time to use it in more practical ways like advertising, production, and learning better ways to deal with your customers? Therefore, the other option is to computerize your work so that you can do a sales analysis to find out which product is giving more sales, and you will be able to change the products that are not selling well. I recommend QuickBooks to do the accounts as that is easy for anyone to learn quickly.

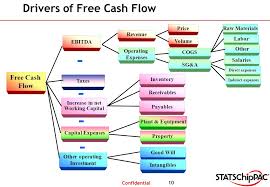

Budget & cashflow

Setting up a budget and cash flow for your start-up is vital, which you should have done at the start of your business. Monitoring cash flow gives you the help to maintain your working capital; if you run out of working capital, you have to start looking for finances from funders. Setting a budget and comparing it with the actual income & expenses helps you control your finances. You have to do these things straight from the start; if not, everything gets out of control, and there is a possibility of facing failure soon.

Final accounts.

To find out the profit or loss in your business, prepare the financial statements at the end of the first financial year. Also, the profit and loss account is essential to determine the tax liability for your tax filing; otherwise, you might underpay or overpay, affecting your business later. If you want to find funding, any lender will ask for your financial statements, cash flow, budget, and business plan for your business.