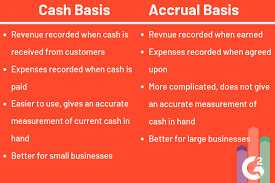

Difference between accounting cash and accrual basis

Most small businesses have a cash basis for many reasons; one is easier for them to record sales and purchases. Besides, you cannot offer your service or product until the cash is received or create records unit the money exchanged.

Whereas an accrual basis, you sell and buy on credit and raise invoices as soon as the sale is made; vital not you will forget the sale and fail to collect the money from your customer. When you buy on credit, you must file and record your receipts. If not, you will forget either to pay or make duplicate payments. You will have a bad credit record for not delivering also might incur interest charges.

If you want to know the profit you made for a month, cash-based accounting gives you the difference between the cash received from income less than the money you paid for purchases. But the accrual basis gave you the profit you made, considering the money you earned and spent regardless of whether you received the capital during the period.

Let me show you the effect of both methods on business.

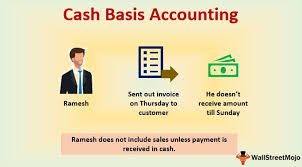

The cash basis method recognizes when cash is received and paid but does not identify accounts payable and receivable.

Most small businesses use this method because it is easy to maintain. A cash basis will not give you an exact amount of profit you made because you might have outstanding bills to pay. Therefore, it is not feasible to make financial decisions with confidence.

Difference between accounting cash and accrual basis

Another advantage is that a business can look at the bank statement and know how much cash is there for the company at a particular time when they try to make any decisions.

However, while cash accounting provides an accurate picture of how much money you have right now, it does not accurately reflect your financial state in the long term. Moreover, that can lead to understated expenses or overstated income.

Another issue on a cash accounting basis is that you might not do well, say in August, but you might receive the cash for the job you did in the previous month. Therefore, when doing your calculation, you might think that you have done well in August but remember that is not correct.

The accrual basis method takes completion of a client’s project as an income regardless of whether the company received the cash. Nevertheless, you would have recorded and issued invoices that go into the records.

More work needs doing involved on an accrual basis, and sometimes you have to use your cash to pay your tax if the customer has not paid you on time. On the other hand, you pay the taxes according to the invoices you issued to customers, but there will be refunds there, affecting your cash flow. Therefore, you consider these when you compute the tax liability. My conclusion is to tell you both methods have bad and good points when you run a business because of this comparison.